I was a keynote speaker at a recent meeting of U.S. and Canadian merchants. Whenever I present, I invite merchants to bring their processing statements and their merchant contracts so I can audit them afterwards. Before starting, I always ask each merchant how often he audits his statements for correctness. Inevitably, merchants who seldom look at their statements are the ones that overpay the most.

Are You Getting What You Negotiated?

Many salespeople bring emotions into the sales process to help get the sale. Some can effectively direct a merchant to focus on what the salesperson wants the merchant to see during their discussions. Auditing your statement enables you to revisit your processing costs away from the emotions and the deft of the salesperson.

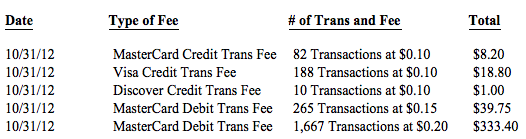

Example 1: Debit vs. Credit

The statement above — which I’ve recreated to make legible — is from a merchant who negotiated what he thought was a great interchange-plus rate with a per transaction fee of 10 cents. However, taking a closer look at the transaction fees reveals that the 10-cent per transaction is for credit cards only. The transaction fee for MasterCard debit cards is 15 cents and 20 cents for Visa debit cards. It doesn’t cost any more for a provider to route a debit card transaction versus a credit card transaction. For this merchant, debit cards represent over 87 percent of all transactions. There were 1,667 Visa debit transactions alone. At 20 cents per transaction, the merchant is paying over $2,000 more per year for Visa debit than if the transactions were priced like Visa credit card transactions. This salesperson definitely knew what he was doing and was in control of the price negotiations.

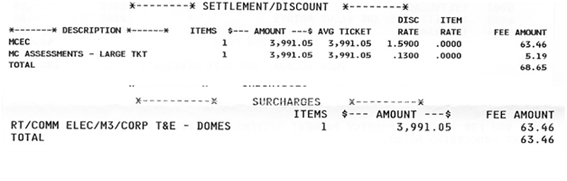

Example 2: Interchange-plus vs. Tiered Pricing

The statement above is from another merchant also thought he negotiated a great interchange-plus rate — see my previous series on that topic. However, he was shocked to learn that he is not even getting interchange-plus pricing. He is on a tiered pricing plan with a base rate of 1.59 percent + 25 cents (the 25 cents not shown). He paid an additional surcharge of 1.59 percent over the 1.59 percent base rate for the MasterCard transaction shown.

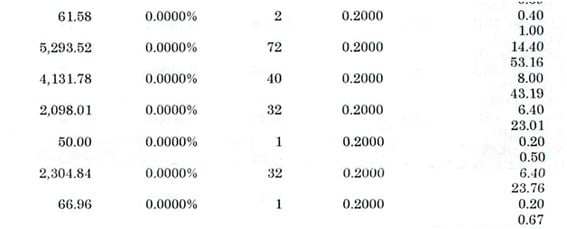

Example 3: PIN Debit vs. Signature Debit

The statement above is from a retail, brick-and-mortar merchant that allows customers to enter a PIN number when they purchase goods and services with a debit card. I have seen this same scenario with debit card pricing for ecommerce merchants and brick-and-mortar merchants that accept debit cards with a signature.

The merchant thought he negotiated a rate of 20 cents over network fees — network fees are the equivalent of interchange for PIN debit — and in fact the contract stated that PIN debit would be at 20 cents over network fees. Keep in mind, PIN debit transactions are subject to the same Durbin Amendment rate reduction and regulations as other debit transactions.

However, looking at the fees shows he is not receiving the lower Durbin Amendment regulated rates. The statement shows (a) the purchase amount for the debit card type at the far left column, (b) the number of transactions in the middle column, and (c) the per transaction fee in the column second from left. The fees in the far left column show the transaction fee followed by the network fee for each debit card type.

For example, there were two purchases on the first card type for a total of $61.58. The merchant was charged 20 cents x 2 transactions = 40 cents. The network fee for $61.58 in sales was $1.00 or 1.62 percent of $61.58. The second card type had 72 transactions for $5,293.52. The fees were 20 cents x 72 transactions = $14.40. The network fees were $53.16 or about 1.00 percent of $5,293.52.

Note that the network fee for each of the above card types is consistently greater than 1 percent. I know from the statement that around 60 percent of the signature debit transactions are receiving the lower Durbin Amendment rates. One would expect about the same percent for the PIN debit transactions. However, with the network fees consistently at or above 1 percent, it’s mathematically impossible for this to be the case. In fact, this merchant is not receiving any of the Durbin Amendment rate reduction for PIN debit. He is overpaying for PIN debit by more the $700 per year.

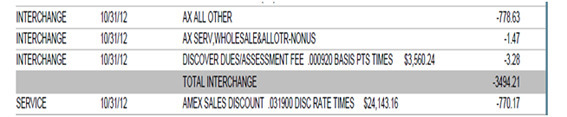

Example 4: Double Charging

The statement above is on the American One Point program from American Express, which offers the One Point program to help merchants. Specifically, the One Point program allows the merchant’s provider to also fund American Express transactions as well as the Visa, MasterCard, and Discover transactions. Therefore, all the American Express processing fees are on the provider’s monthly credit card processing statement versus receiving a separate statement from American Express.

In this case, American Express charged 2.89 percent + 15 cents = $778.63 for all but one of the transactions. There was one transaction for 3.29 percent + 15 cents = $1.47.

However, the provider is also charging a 3.19 percent Amex Sales Discount rate in addition to the processing fees charged by American Express. This additional fee = $770.17. I assume this is an order-entry error by the provider. Nonetheless, this merchant never audited his statement to determine if he was being charged correctly for all his processing. This error has been costing this merchant over $9,000 per year.

The Good News

All the above issues can be corrected. However, a merchant needs to first know these issues exist and that is done by doing a detailed audit of the statement.

Summary

- Merchants must periodically audit their statements in detail to ensure they are being charged correctly.

- Make sure you know what you negotiated.

- Do not assume that what you negotiated is what you are getting.

- Do not assume the provider process is error-free.