Having a good accountant is important to the success of every small business. But do you really understand all the terms in the documents your accountant prepares? Relying too heavily on financial professionals can limit your understanding of the underpinnings of your company. Don’t worry; you don’t need an accounting degree to master a basic understanding of financial statements. Following is a primer to help manage your business.

The purpose of financial statements is to show a company’s financial status over a certain period of time. Usually statements are presented on a monthly, quarterly and annual basis. Quarterly statements, when compared to one another, can show trends and alert business owners to problems that require immediate attention.

The three key financial statements for small businesses are:

- Balance Sheet;

- Income Statement;

- Cash Flow Statement.

Balance Sheet

The balance sheet comprises assets and liabilities plus the owner’s equity (net worth) divided into two financially balanced sides. The figures are accurate as of the last day of the reporting period. Assets are always on the left side with liabilities and equity on the right. Sometimes assets are presented above liabilities and equity. Equity is equal to assets minus liabilities; a company’s assets have to balance the sum of its liabilities and owners’ equity.

Assets are company-owned items that have value and can be sold or used in production. They encompass both physical property and intangibles such as patents. Assets are organized on the balance sheet in descending order of liquidity (how easy it is to covert into cash), as follows.

- Cash. Readily available funds you can use now.

- Accounts receivable. Money owed to you for items you sold but haven’t yet received payment.

- Inventory. Raw materials, work-in-process goods, and finished goods that are ready for sale. Inventory is an example of a “current asset,” something a company expects to convert to cash within one year.

- Prepaid expense. For goods and services to be received shortly or for a contracted period. Insurance is an example.

- Fixed Assets. Examples include machinery, office equipment, office building.

Accounts receivable can balloon if customers take a long time to pay. It’s important to ensure that the majority of customers pay within your standard terms. In bad economic times, customers stretch out the payment time and a company needs to manage the receivables to ensure adequate cash flow.

The turnover of inventory represents one of the primary sources of revenue and earnings. Possessing a lot of inventory for long periods of time is undesirable because it results in increased storage, obsolescence, and spoilage costs. However, if a business keeps too little inventory it runs the risk of forfeiting potential sales. Paying attention to the balance sheet and comparing sequential statements can help business owners determine an optimal amount of inventory.

Liabilities are obligations that a company owes to others. They can include bank loans, rent, money owed to suppliers for raw materials, payroll, and taxes owed to the government. Liabilities also include obligations to provide goods or services to customers in the future. “Current liabilities” are obligations a company expects to pay off within the year. Long-term liabilities are obligations due in more than one year.

The most common form of liability is accounts payable. This is money that a company owes to vendors for products and services purchased on credit. This item appears on the company’s balance sheet as a current liability, since the expectation is that the liability will be fulfilled in less than a year. Taxes, accrued expenses, debt, and deferred revenues are other examples of liabilities.

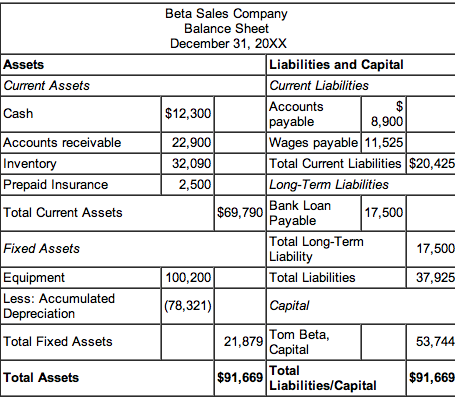

Sample balance sheet.

Income Statement

An income statement is a report that shows how much revenue a company earned over a specific time period. It also presents the costs and expenses associated with earning that revenue. The first line of the income statement reflects the total amount of money earned from sales of products or services before deducting expenses. This top line is often referred to as “gross revenue” or “sales.” The next line consists of money the company doesn’t expect to collect because of sales discounts, merchandise returns or shrinkage. The last line of the statement usually shows the company’s net earnings or losses — with returns and allowances deducted.

Next are several lines that represent various kinds of operating expenses. Typically the line after net revenue presents the costs of sales. This number is the amount of money the company spent to produce the goods or services it sold during the accounting period. This amount is subtracted from net revenue, resulting in a subtotal called “gross profit” or “gross margin.”

The next segment presents operating expenses. These are costs that support a company’s operations but are not linked directly to production. Salaries and marketing outlays are examples of operating expenses.

Depreciation, a method of allocating the cost of a tangible asset over its useful life, is also deducted from gross profit. Businesses depreciate long-term assets for both tax and accounting purposes.

The operating profit, also called income from operations, is the result after all operating expenses have been subtracted. Next, companies must tally interest income and interest expense. Companies derive interest income from keeping their excess cash in interest-bearing savings accounts, money market funds, and other liquid investments. Interest expense is the cost of borrowing money. Interest income and expense are then added or subtracted from the operating profit, resulting in operating profit before income tax.

Last, income tax is subtracted and the result is the bottom-line “net profit” (also called “net income”) or “net loss.” This is how much a business earned or lost during the accounting period.

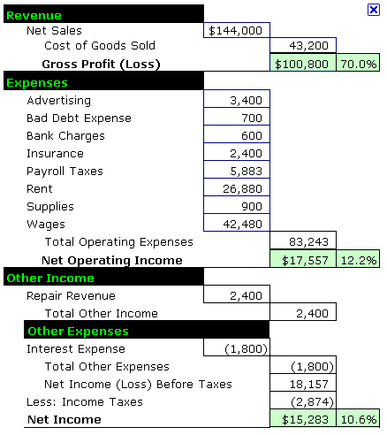

Sample income statement.

Cash Flow Statement

For a small business, the cash flow statement may be the most important because a company has to have enough cash on hand to pay its expenses. This document gives a snapshot of the company’s inflows and outflows of cash over time rather than at the end of an accounting period. However, the last line of the cash flow statement shows the net increase or decrease in cash for the period. Cash flow statements are usually divided into three parts.

- Operating activities. The first part of a cash flow statement analyzes a company’s cash flow from net income or losses. This section reconciles the net income as shown on the income statement to the actual cash the company received from and used in its operating activities. To accomplish this, it adjusts net income for any non-cash items (such as depreciation or goodwill) and adjusts for any cash that was used or provided by other operating assets and liabilities. Good cash flow management means delaying payables as long as possible, while trying to accelerate collection of money owed to the company.

- Investing activities. The second part of a cash flow statement shows the cash flow from all investment activities, which generally include purchases or sales of long-term assets. If the company sold some investments from an investment portfolio, the proceeds from the sale would be included as a cash inflow from investing activities.

- Financing activities. The third part of a cash flow statement shows the cash flow from all financing activities such as a bank loan. Proceeds of a loan would show up as an inflow. Likewise, paying back a bank loan would show up as an outflow.

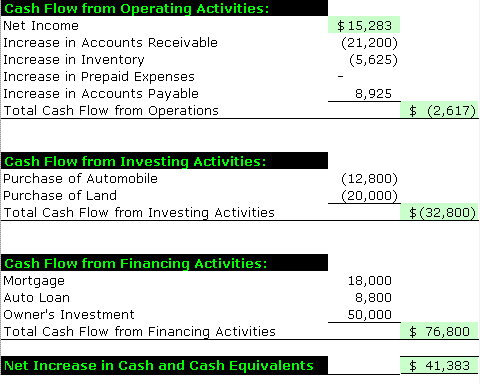

Sample cash flow statement.

Conclusion

A useful website for financial information is Investopedia.com, which provides simple definitions and explanations of financial terms, Also, be aware that publicly traded companies have more complex financial statements, including a shareholders’ equity section.