Visa, MasterCard, and Discover generally change rates and terms in April and October. However, they can make changes at other times during the year, as will happen this year. Unfortunately, over the years, some providers have taken advantage of these changes by increasing their rates and fees ostensibly because of these card association and company changes. However, many of the provider increases were well beyond the actual card associations and company changes.

Below is a reprint of a notification one provider sent merchants last year regarding the October 2012 changes.

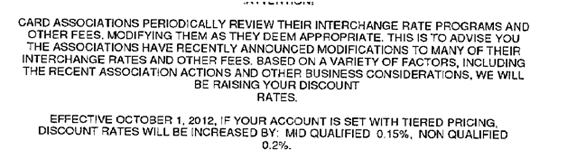

Card Associations periodically review their interchange rate programs and other fees. Modifying them as they deem appropriate. This is to advise you the associations have recently announced modifications to many of their interchange rates and other fess. Based on a variety of factors, including the recent association actions and other business considerations, we will be raising your discount rates.

Effective October 1, 2012 if your account is set with tiered pricing discount rates will be increased by: Mid Qualified 0.15 percent Non Qualified 0.2 percent.

Credit cart rate change notice example.

This provider increased Mid-Qualification and Non-Qualification rates for its merchants on tiered pricing. Basic reward cards and other card types generally fall into the Mid-Qualified rates. Commercial cards, higher end reward cards, and transactions that do not meet qualification requirements generally fall into the Non-Qualified rate.

When you read the above rate increase notice it may feel like Visa, MasterCard, and Discover are the culprits. However, the reality is that they did not implement any changes that justified these rate increases. In fact, some of their changes in October actually lowered certain interchange rates.

April Changes Were Minor

The actual changes in April were minor for most merchants.

First, understand that the card associations and companies only implemented a few general changes in April. Most of those changes were semantics with Visa creating a new interchange category for commercial pre-paid cards and MasterCard renaming its enhanced value for small business interchange. Any rate changes with these programs will have a very minor effect on the average merchant — if any effect at all.

The one change that needs brief mentioning is MasterCard’s increase of its “Acquirer Support Fee.” This fee applies when a customer purchases goods and services from a U.S. merchant and pays with a MasterCard issued outside the U.S. MasterCard increased its fee in April from 0.55 percent to 0.85 percent. This means that for every $1,000 purchased with a non-U.S. issued card, MasterCard will now charge $8.50 instead of the previous $5.50. Transactions using MasterCard cards issued in the U.S. are not charged this fee.

To understand how your provider is implementing these changes, you first have to review any notifications on the previous statements as well as the statement for April activity. The above notification for the October 2012 changes was on a statement merchants received in September for their August processing activity. You will generally find provider notifications on the last page of the statement.

Often the notices can seem somewhat cryptic, as with the example below. A provider recently sent this notice to its merchants regarding the April 2012 changes.

Effective May 1, 2013, all international MasterCard consumer programs for card not present businesses will move from rate 2 to rate 3. For card present businesses, MasterCard international electronic programs will move from rate 2 to rate 3 and all other international MasterCard consumer programs will move from rate 3 to rate 4 in response to pricing changes received from MasterCard.

If you do not understand the change, have your staff contact the provider to obtain specific information on precisely how you will be impacted. However, there should not be any across-the-board rate increases due to the Visa and MasterCard April changes as was seen in the October 2012 notice shown before. If your provider is implementing an across-the-board rate increase it is not because of any changes made by Visa and MasterCard in April.

Below is a more appropriate notice one provider sent its merchants regarding the April 2013 change. This notice specifically notes the 0.30 percent increase by MasterCard and also states that the fee will be passed along to the merchant, which is fair.

Effective April 1, 2013 MasterCard will increase the Acquirer Processing Support Fee (APSF) by 30 basis points (.0030) for transactions paid for with a card issued outside the United States and settled in US dollars. This increase will be passed along to you should it apply to a given transaction.

Keep in mind that you can also have a professional company audit your statements for rate or fee changes if you do not feel comfortable doing so yourself. However, make sure the company is not affiliated with or receiving compensation from any providers. There are some good companies willing to conduct free and confidential audits. The audit should be conducted to educate you on your current processing situation. It should not be done to try to convince you to change providers.

Summary

- Some providers have taken advantage of card company changes by increasing rates.

- The April 2013 changes are minor for the average merchant.

- Take the time to audit your statement or have an independent professional audit it.